If you’re a regular reader you’ll know I agreed to take on 22seven’s money-saving GY$T challenge a few weeks earlier. You can learn more about the app (amazing!) and more about the challenge over here, but if you’re already in the loop keep reading.

Get around for less

The first task of my seven part challenge was to see if I can bring down my travel costs and a suggestion was to find out if, when you take Cape Town’s horrific street parking costs into consideration, it wasn’t perhaps cheaper to grab an Uber instead of use my car. As it turns out it, it wasn’t. I worked this out by driving to the point I was running on fumes. I then bought one hundred rand’s worth of petrol (it got me 7,8 litres, that’s R12,83 per litre) and set my odometre to zero. Once I’d driven it all out I saw I’d managed to drive 84km on it, meaning using my car costs me a mere R1,19 per km.

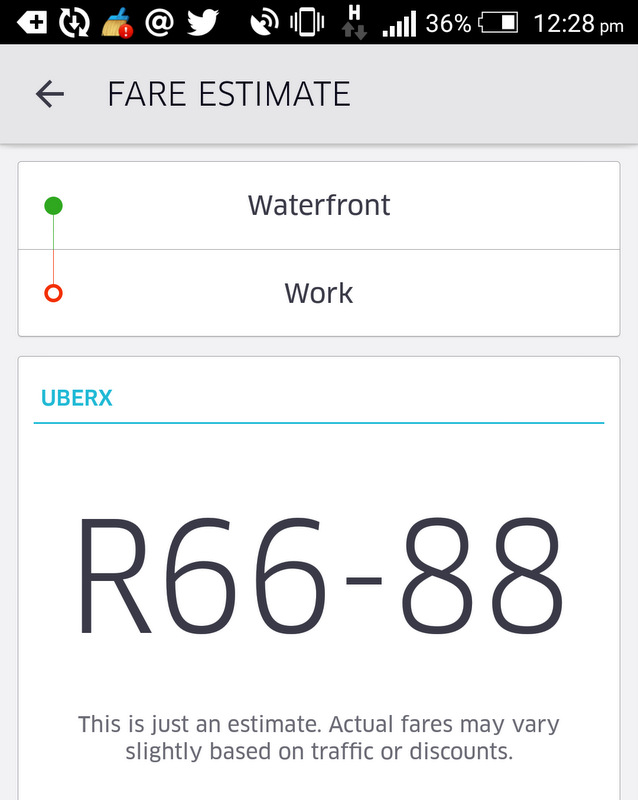

Keen on yet more math? If I drive to the Waterfront from my flat in Observatory Uber wants to charge me R66,88, so a return trip would be R133,76.

If I took my car, it would cost me R26,60 return (11,2km x R1,19 = R13,32 x 2) + R30 (3 hours worth of parking) which equals just R56,60.

So, the bottom line is to keep driving, but share lifts wherever possible and be more aware of how I plan my week by planning errands in clusters to avoid multiple trips.

Estimate saving in a year: None. Keep on drivin’ chica!

Bust my bank fees

Despite having a very basic savings account with ABSA, my banking fees are crazy high. Before getting 22seven I’d never noticed as I’d look at my statement and would just see the odd R8 taken off there, the inexplicable R35 there. It didn’t feel like it could add up to anything shocking but thanks to the app I can see I’m paying an average of R230 per month. That’s R2 760 per year! What?!

That’s all I needed to hear to change banks.

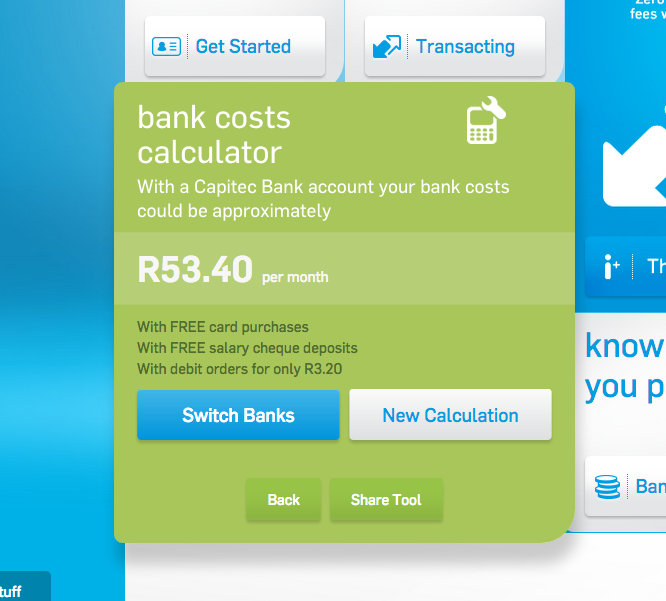

While ABSA offered to relook at things for me after seeing my tweet, they could only offer me a new account that caps my fees at R99 but this means I still have to get a new bank account number and go through the las of changing my debits and what not. So if I’m going to sikkel with all that, I might as well move all the way to Capitec. According to their calculator, I’ll probably pay just R53,40 per month, maybe even less.

Estimate saving in a year: R2119,20.

Put the sure into insurance

I’m currently using King Price as my insurers and I’m really happy with them. I pay R447 to cover my Kia and MacBook Air and couldn’t find a place that could beat it to my satisfaction so happiness all round there. For the record, every interaction I’ve ever had with King Price has been a good one, including the two times I’ve called on their roadside assistance.

Estimate saving in a year: None. I made a good choice here.

Do a little subscription subtraction

I took a long hard look at my ‘subscriptions’, the things I regularly paid for each month, and found them to be my internet package (Afrihost), gym membership (Virgin Active), cellphone contract (Cell C) medical aid (Discovery Coastal Core).

I’m currently locked into a nightmarish relationship with Cell C from which there’s no escape so let’s not go there. I did a few online comparisons and found my medical aid and internet package where still serving up the best prices for what I wanted. Gym however, is an issue. I’ve been with blerrie Virgin for yonks and haven’t set food inside their gym for two years as I have one within my apartment complex.

Belonging to Virgin, the club I never go to, sets me back R350 a month so I should just cancel it, right? The reason I don’t, however, is because I’m always telling myself I might want to pop in for a class. But I never do. So what am I doing? Arrrgh! I’ve yet to do it as I’ve been swamped but I plan to call the club and find out what kind of new fees I’d be looking at if I cancelled and then rejoined at a later stage. I’m worried that, as a ‘new joiner’ I’ll be asked to cough up R500 a month or something stupid. So ja, let’s watch this space.

Estimate saving in a year: R4 200 (if I man up and do it).

Deload my lunch

I spend a disgusting amount on eating out. Disgusting. A lot of this has been minimised by finding ‘something free to entertain myself’ (see below) but I’ve managed to cut my grocery spend dramatically too by shopping like an American dooms day survivalist. How? I cruise Checkers’ voucher app as well as Woolies’ and Fruit & Veg City’s specials pages and when I spot something that freezes well or can last forever in a cupboard I buy it in bulk.

I now also cook more meals at home, divvie them up and freeze them. My beloved Pioneer Woman’s banting-friendly chilli recipe is a particular fave and whipping it up costs around R120 which works out to R12 a meal as you’ll easily get 10 servings. Also, when I spotted Woolworths’ family-sized lasagna marked down to just R75 I bought ten million, cut them into four and then revelled in my R18,75-per-meal cleverness for months.

Also, rather than perpetually stock up on fresh goods that just rot in my fridge because I’m almost never home, I’ve become more aware of buying fresh every couple of days as opposed to every week. I also like using Supercook to search for recipes by the ingredients you already have in your fridge so you can use everything up economically before hitting the shops once more.

Last but not least, I’ve managed to kick my KFC cappuccino addiction. I live right next door to Colonel Saunders’ deep fried shack o’ evil and got into a groove where I’d buy a R14,90 coffee five days a week to the merry tune of R298 a month. I’ve now switched to Nescafe instant cappuccino sachets (R49,95 for 10) which means I’m now only parting with R99,99 a month and saving almost R200 in the process.

Estimate saving in a year: Kicking my KFC cuppa habit alone has saved me R2 400.

Find something free to entertain myself

Ah, this was easy. Now that I’m hiking outdoors and running on the prom with friends I consider this exercise and entertainment. Also, now when friends want to hook up for dinner, I suggest they rather join me for a walk outdoors. Alternatively, I eat dinner at home and then join them for a drink. This latter teensy shift has made a huuuge difference to what I spend on eating out. A restaurant lunch or dinner is no-longer my default ‘let’s hook up’.

Still, if I do eat out, I’m now quick to suggest a restaurant from the list of those on my Entertainer app. It costs R395 (but I got it for around R300 when they had a special) and then you can eat at a host of restaurants (up to three times each) and use a voucher that sees you buy one main and get another to the value or less for free. It’s not technically ‘doing something for free’ but this year’s seen me use 21 vouchers and if we assume a main is R100, it’s saved me a solid R1 050.

Estimate saving in a year: Let’s not even go there. My brain can’t handle this kind of math. That’s why I have that fabulous 22seven app.

Cash it to cap it

Cash it to cap it essentially means drawing a set amount of cash and sticking to it as opposed to running around with your ‘bottomless’ card. When you’ve got your card in your wallet, saying yes to dessert is easy, even though you promised yourself you’d only have a starter and a main before you left the house. I’m also the person who usually insists on getting the whole bill when it comes round. ‘No, no! It’s on me! You can get the next one’. (But I despise it when other people pay for me, so that time pretty much never, ever comes.)

So, did capping it work? Yep, it did. It really did. I’d still take my credit card along with me as I’m uncomfortable without it (What aliens land and want to whisk me off to an intergalactic ball? Surely I’d need to buy an emergency Star Princess dress en route? Life throws you curve balls, ok?!) but physically having a certain amount of rands in my pocket was a solid budget reminder. It’s now something I’m applying to other things. For example, I’ll draw a certain amount in cash to be spent on groceries, divvie it up per week and then keep it in an envelope in my wallet. Watching the pile thin out as the days go by as opposed to mindlessly swiping really does make you more aware of your spend.

Estimate saving in a year: Again, I have no clue how to calculate my exact savings here. But it’s a lot. I’ve been known to get blind drunk and hand out my card screaming ‘the next bottles on me! All my friends know my PIN number. I’m very lucky I pick them well.

So, having made these small changes and if I toss my stupid Virgin Active membership, I can save a total of R8,719 in a year. Did you hear that mense? Almost nine freakin’ thousand rand! And this is excluding what I’m saving now that I’m getting a grip on my penchant for eating out. That’s two grand shy of a package holiday involving an eight night stay in Phuket. (I know this ‘cos I’ve just checked.)

If you’re keen to get your $hit together the way I have, download the 22seven app and wise up about exactly where your moolah’s going. For me, it’s been a life (and serious cash) saver.

Love, love

Leigh

awesome. Have been looking for an app like this

Also a 22Seven user, and it has been mostly useful for managing a unified view of both my & my husband’s multitudinous accounts.

Ahh, the perpetual gym contract dilemma. Just cancel it already. I’ve been trying to convince my hubby to get rid of his for years, too. He has the same fear you do, and he’s been to the gym once in the last 3 years. I’m going to do the math like you did and convince him to GHisST :).

Just wanted to point out that the Uber fare estimate is a range, not a decimal. It would cost between R66.00 and R88.00 for the ride, not R66.88 as you’ve used it. However, having lived in Obz myself, I know how frustrating it is that the MyCiti bus routes end in Woodstock and the Southern suburbs are completely under-served.

The train is cheap but a bit manky and infrequent, however the taxis up Main Road into town are pretty good and only R6. So for a year I used a combination of the 3 – taxis, MyCiti and Uber.

I’m also with Capitec already and I adore my bank and my seriously low fees. Their in-branch service is amazing, too. I no longer hate the thought of going into the bank. Make the switch! It’s worth it!

How have I only see this comment now? Thanks so much for this. I had no clue Uber was a range as opposed to a figure. Ja, I’ve decided I’m getting rid of my gym contract on Monday and going to sign up with Capitec the moment I get free time to step into a branch. ABSA’s eaten up way too much of my cash.

I too have been going through a similar exercise and made a few discoveries, when FNB launched their ebucks, great banking at low cost initiative and begged you to make the switch…I took the bait but did not make the full switch, I did apply for a credit card to test the waters, for a while, I earned bucks and qualified for lounge access with my platinum card…well all that changed a few months ago when they moved the goal posts yet again and all of a sudden you had to have both cheque and credit card in order to earn ebucks and qualify for lounge access. The best bait and switch move I have seen in years. Thankfully I stayed with trusty SBSA and only used the FNB as a cash card and settled at month end, I am able to cancel and save the almost R300 a month in bank fees and R200 in ebucks ‘access’ fees…lesson learnt…